Last June, I wrote a post about the growing number of bank closures. I checked the FDIC web site and created the following tally. By June 2009, there had been 45 bank closures, and the year was only half-done.

So, today, I thought I'd update that Bank Closure List. Using the information from the FDIC bank failure list (and checking myself against a table of bank closures created by CNN.com), here's what I found:

Oct to Dec 2000 - 2

2001 - 4

2002 -11

2003 - 3

2004 - 4

2005 - 0

2006 - 0

2007 - 3

2008 -24

2009 -- 140

(Jan - June 28 = 45; June 29 - December 31 = 95)

2010 - 37 so far this year

January - March 23 - 37

Showing posts with label investing money tips. Show all posts

Showing posts with label investing money tips. Show all posts

March 24, 2010

March 4, 2009

FDIC Letter Threatens FDIC Insolvency - This is Big News But What Does It Mean to You?

Today, there was big news that maybe isn't getting the attention it deserves: the head of the FDIC has sent a letter to banks and thrifts across the country, explaining to their CEOs that the FDIC must raise its fees, as well as be paid the big surprise extra premium payment that it voted for itself last week, otherwise the FDIC will become insolvent in a matter of months.

That the FDIC is even hinting that it may be insolvent at any time is spooky stuff, and I'm thinking more than adequate to start some folk on a run to their banks.

That the FDIC is even hinting that it may be insolvent at any time is spooky stuff, and I'm thinking more than adequate to start some folk on a run to their banks.

September 28, 2008

The FDIC Watch List: Should You Pull Your Money Out of Your Bank?

Yesterday, I was buying groceries at the local HEB and as usual, I whisked my debit card through the little black box, inputed my passcode, and waited for my receipt ... only to have the cashier ask me to run the card again - it hadn't gone through.

Now, I always know the balance in my checking account and my first thought was Identity Theft! But with today's economic mess, right on its heels was my second thought, My Bank's Gone Under!

Turned out that the cashier hadn't pressed a button, and my second attempt worked just fine ... but I got to wondering about the security of my bank deposits and went surfing on the web to investigate.

Here's what I learned:

1. On August 26, 2008, FDIC chairwoman Sheila Barr had a press conference where she announced that 117 banks were now on the FDIC "watch list," up from 90 banks at the beginning of the year. So, they've added 27 banks to the list in the past 8 months. It's the highest number in the past 5 years.

2. At this press conference, the head of the FDIC didn't release the actual list. The feds don't want to give out that actual information, because they are afraid that depositors will read the list, and run to take their money out of those banks on the list. The FDIC Watch List is as big a secret as the recipe for Kentucky Fried Chicken, it seems.

Of course, there's not enough cash in these banks to cover a run - banks loan money, that's how they make a profit (think Jimmy Stewart in It's A Wonderful Life) ... and the FDIC would have to step up and provide cash to cover the depositors' demands - and that's true for the healthiest of banks. The problem these days, apparently, is that loan business hasn't been profitable.

3. So far this year, 13 banks have failed in the US (WaMu was number 13). Only three (3) banks failed in 2007. A banking analyst interviewed by ABCNews opines that we'll see over 100 bank failures by the end of 2009, although most will be "small institutions."

4. LACE Financial (a company that monitors the banking industry) reports that for commercial and savings banks, net income was 74% lower in the 2nd quarter of 2008 (April, May, June) than it was for the first quarter (Jan, Feb, March) -- and that the 2nd quarter of 2008 was 87% lower than it was last year, in 2007. This is industry-wide: sounds like banks are not making any money, huh?

The FDIC Watch List -- and Other Bank Ranking or Watch Lists

5. There are companies or groups that rank the safety of banks, independently of the FDIC. These include:

So, with this scary news, what do you do? Do you pull your money?

6. If you've got money in a bank, the first thing you should know is whether or not your money is deposited at an institution that is protected by the FDIC. Go check the FDIC online list to find out. Whether or not the FDIC is strong enough to handle the hits it may be facing is one issue (watch for an upcoming post on that concern)but not having your money in an account that's even offered FDIC protection is another. If you're banking, then you want FDIC protection.

7. Next, remember that the FDIC doesn't cover everything -- the contents of your safety deposit box aren't covered; any amounts over $100,000 in your checking account and $250,000 in your IRAs aren't covered; money market funds, etc. are not covered. Move your funds around, as needed, to make sure you are within the guidelines -- and if you've got cashed stashed in those safety deposit boxes, think about whether that's the best place for it to be.

8. If your bank fails, and it's protected by the FDIC, then you may face a couple of days where access to your account might be hampered. Keep some cash on hand, if you can, to cover the necessities -- diapers, gas, things like that.

9. If you choose to take your money out of a bank, then you're faced with difficulties. First, how to protect it. That's one reason for a bank, right? Fire, burglary - these are real threats to your nest egg. Also, you're going to face a difficult time paying your bills if you've been accustomed to writing a check, or paying online. You can pay by money order, but it's a hassle. Maybe you stash cash and keep an account open at an institution you consider safe, just to pay bills - keeping as little cash there as possible, depositing right before you pay the monthly invoices?

What does all this mean?

10. Here's LACE Financial's outlook:

11. For me, this means that this Fall will be bad, but next year will be worse -- unless some major events transpire. In my surfing around, I've started to see the phrase "slow depression," mentioned quite a bit. I'm going to pray and study a lot, take it a day at a time, and a step at a time, and I'm going to read those folk over at the Daily Reckoning, among others. They've been warning about this crisis for a long time now.

Fear is Your Enemy

Fear can hurt you, even destroy you. This is no time to panic, it's time to be smart. You will get through this. Everything is going to be alright -- maybe not the same, but you and yours will be okay. And, if you're already in the process of living a simplicity lifestyle, you're ahead of the game.

For more information:

What is Simplifying? Should You Do It?

Starting to Simplify - Step 1

Starting to Simplify - Step 3

Are You Brave Enough to Read Empire of Debt?

Now, I always know the balance in my checking account and my first thought was Identity Theft! But with today's economic mess, right on its heels was my second thought, My Bank's Gone Under!

Turned out that the cashier hadn't pressed a button, and my second attempt worked just fine ... but I got to wondering about the security of my bank deposits and went surfing on the web to investigate.

Here's what I learned:

1. On August 26, 2008, FDIC chairwoman Sheila Barr had a press conference where she announced that 117 banks were now on the FDIC "watch list," up from 90 banks at the beginning of the year. So, they've added 27 banks to the list in the past 8 months. It's the highest number in the past 5 years.

2. At this press conference, the head of the FDIC didn't release the actual list. The feds don't want to give out that actual information, because they are afraid that depositors will read the list, and run to take their money out of those banks on the list. The FDIC Watch List is as big a secret as the recipe for Kentucky Fried Chicken, it seems.

Of course, there's not enough cash in these banks to cover a run - banks loan money, that's how they make a profit (think Jimmy Stewart in It's A Wonderful Life) ... and the FDIC would have to step up and provide cash to cover the depositors' demands - and that's true for the healthiest of banks. The problem these days, apparently, is that loan business hasn't been profitable.

3. So far this year, 13 banks have failed in the US (WaMu was number 13). Only three (3) banks failed in 2007. A banking analyst interviewed by ABCNews opines that we'll see over 100 bank failures by the end of 2009, although most will be "small institutions."

4. LACE Financial (a company that monitors the banking industry) reports that for commercial and savings banks, net income was 74% lower in the 2nd quarter of 2008 (April, May, June) than it was for the first quarter (Jan, Feb, March) -- and that the 2nd quarter of 2008 was 87% lower than it was last year, in 2007. This is industry-wide: sounds like banks are not making any money, huh?

The FDIC Watch List -- and Other Bank Ranking or Watch Lists

5. There are companies or groups that rank the safety of banks, independently of the FDIC. These include:

- Bauer Financial (go to their site, find your state or your bank)

- LACE Financial (LACE doesn't offer up its "Watch List" online for free; however, it does report that in the second quarter of 2008, its D List (next to the lowest ranking) rose by 40% and its E list (lowest ranking) rose by 64%. Right now, LACE has 684 banks on its D List, and 490 institutions on its E list. And, LACE also finds its List to be more accurate than the FDIC Watch List, because the FDIC List has to await the bank examination process and the CAMEL ratings - the LACE list is simply faster to finalize. )

- VeriBanc (you're invited to call and chat with them -- but there's a fee)

- The Implode-O-Meter (a non-industry participant that has created its own ranking system and website list -- "implode," defined as "the "imploded" status is somewhat subjective and does not necessarily mean operations are ceased permanently: it can mean bankruptcy filing, temporary but open-ended halting of major operations, or a "firesale" acquisition. The Companies include all types (prime, subprime, or a mix of both; retail or wholesale; subsidiaries and entire companies). Note: Companies listed here may still be operating in some capacity; check with them before making assumptions." According to this Watch Group, 286 major financial institutions have "imploded" in the US over the past year and a half (since 2006). )

So, with this scary news, what do you do? Do you pull your money?

6. If you've got money in a bank, the first thing you should know is whether or not your money is deposited at an institution that is protected by the FDIC. Go check the FDIC online list to find out. Whether or not the FDIC is strong enough to handle the hits it may be facing is one issue (watch for an upcoming post on that concern)but not having your money in an account that's even offered FDIC protection is another. If you're banking, then you want FDIC protection.

7. Next, remember that the FDIC doesn't cover everything -- the contents of your safety deposit box aren't covered; any amounts over $100,000 in your checking account and $250,000 in your IRAs aren't covered; money market funds, etc. are not covered. Move your funds around, as needed, to make sure you are within the guidelines -- and if you've got cashed stashed in those safety deposit boxes, think about whether that's the best place for it to be.

8. If your bank fails, and it's protected by the FDIC, then you may face a couple of days where access to your account might be hampered. Keep some cash on hand, if you can, to cover the necessities -- diapers, gas, things like that.

9. If you choose to take your money out of a bank, then you're faced with difficulties. First, how to protect it. That's one reason for a bank, right? Fire, burglary - these are real threats to your nest egg. Also, you're going to face a difficult time paying your bills if you've been accustomed to writing a check, or paying online. You can pay by money order, but it's a hassle. Maybe you stash cash and keep an account open at an institution you consider safe, just to pay bills - keeping as little cash there as possible, depositing right before you pay the monthly invoices?

What does all this mean?

10. Here's LACE Financial's outlook:

The financial condition of the U.S. banking system is rapidly deteriorating as the increased number of banks on the LACE Watch List reflects. It appears to us that nineteen of these banks should have already been closed and thirty-two other banks require capital infusions or regulatory assistance. A major cause of failure for several of these banks will be due to high concentrations in real estate construction lending. Given the likely resource constraints of Federal regulators, we would expect a measured closure rate of approximately ten banks by the end of 2008 with failure rates accelerating after the first of the year. As such, LACE Financial maintains a negative outlook for the U.S. banking system.

11. For me, this means that this Fall will be bad, but next year will be worse -- unless some major events transpire. In my surfing around, I've started to see the phrase "slow depression," mentioned quite a bit. I'm going to pray and study a lot, take it a day at a time, and a step at a time, and I'm going to read those folk over at the Daily Reckoning, among others. They've been warning about this crisis for a long time now.

Fear is Your Enemy

Fear can hurt you, even destroy you. This is no time to panic, it's time to be smart. You will get through this. Everything is going to be alright -- maybe not the same, but you and yours will be okay. And, if you're already in the process of living a simplicity lifestyle, you're ahead of the game.

For more information:

What is Simplifying? Should You Do It?

Starting to Simplify - Step 1

Starting to Simplify - Step 3

Are You Brave Enough to Read Empire of Debt?

June 24, 2008

Reverse Mortgages - Don't Get Scammed

You've seen them. Seems like there are more and more advertisements for reverse mortgages every day on TV and in the paper. They make reverse mortgages sound like something that's almost too good to be true. It might be: the government reports that reverse mortgage scams are on the rise.

Before you even contact one of these companies, go to the US Department of Housing and Urban Development website and read everything they provide: some of these companies are asking people to pay for this free information. Don't pay for what's free! For example, HUD offers the "Top Ten Things to Know About Reverse Mortgages" at its site.

AARP has lots of good info on its website, too. AARP has information on how to decide between selling your home outright and opting for a reverse mortgage (the pros and cons) as well as five questions to ask yourself before considering a reverse mortgage.

Finally, the Federal Trade Commission is a great source of free information about reverse mortgages.

The FTC also warns Americans:

"Be cautious if anyone tries to sell you something, like an annuity, and suggests that a reverse mortgage would be an easy way to pay for it. If you don’t fully understand what they’re selling, or you’re not sure you need what they’re selling, be even more skeptical.

"Keep in mind that your total cost would be the cost of what they’re selling plus the cost of the reverse mortgage. If you think you need what they’re selling, shop around before you buy.

"No matter why you decide to take a reverse mortgage, you generally have at least three business days after signing the loan documents to cancel it for any reason without penalty. Remember that you must cancel in writing. The lender must return any money you have paid so far for the financing."

Before you even contact one of these companies, go to the US Department of Housing and Urban Development website and read everything they provide: some of these companies are asking people to pay for this free information. Don't pay for what's free! For example, HUD offers the "Top Ten Things to Know About Reverse Mortgages" at its site.

AARP has lots of good info on its website, too. AARP has information on how to decide between selling your home outright and opting for a reverse mortgage (the pros and cons) as well as five questions to ask yourself before considering a reverse mortgage.

Finally, the Federal Trade Commission is a great source of free information about reverse mortgages.

The FTC also warns Americans:

"Be cautious if anyone tries to sell you something, like an annuity, and suggests that a reverse mortgage would be an easy way to pay for it. If you don’t fully understand what they’re selling, or you’re not sure you need what they’re selling, be even more skeptical.

"Keep in mind that your total cost would be the cost of what they’re selling plus the cost of the reverse mortgage. If you think you need what they’re selling, shop around before you buy.

"No matter why you decide to take a reverse mortgage, you generally have at least three business days after signing the loan documents to cancel it for any reason without penalty. Remember that you must cancel in writing. The lender must return any money you have paid so far for the financing."

October 10, 2007

Retiring in Mexico

More and more news reports are covering the rise in Americans retiring in Mexico. This is due in part to the lower cost of living, as well as the lower costs of medical and dental care and nursing home expense. It's also due in part to the Mexican people themselves: their loving attitudes toward family, and friendly acceptance and assistance to expatriates, makes Mexico a welcoming place for many Seniors.

More and more news reports are covering the rise in Americans retiring in Mexico. This is due in part to the lower cost of living, as well as the lower costs of medical and dental care and nursing home expense. It's also due in part to the Mexican people themselves: their loving attitudes toward family, and friendly acceptance and assistance to expatriates, makes Mexico a welcoming place for many Seniors. For more information on retiring in Mexico, check out these sources:

Mexperience

The People's Guide to Mexico

Gadling

ExpatForum - Mexico

MexConnect

Transitions Abroad - Mexico

June 20, 2007

Site to See: Debt-Proof Living

Debt-Proof Living may be known to some of you as Cheapskate Monthly: the site has been revamped and renamed. Written by the money editor for Women's Day, the site is busting at the seams with financial tips - along with personal notes from Mary Hunt about her quest for a debt-free lifestyle.

Debt-Proof Living may be known to some of you as Cheapskate Monthly: the site has been revamped and renamed. Written by the money editor for Women's Day, the site is busting at the seams with financial tips - along with personal notes from Mary Hunt about her quest for a debt-free lifestyle. The Hunts have simplified their lives, and their initial motivation was financial. This may not be true for everyone (my initial motivation to simplify was not based upon money, for example), but Mary Hunt has a lot of good advice and encouragement for anyone in the midst of seeking a simpler life.

It's a great site. I think you'll find things there that you will use.

May 19, 2007

Online Calculator: Early Mortgage PIF

There's wisdom in the saying "in consistency is power," and if you're willing to add a couple of hundred bucks to your mortgage payment every month, you can pay off the house a lot faster than you think.

To figure out how much -- and how fast -- check out this online PIF calculator. Just $100/month can literally cut years off your payment schedule -- and save you $1000s in interest.

September 9, 2006

Very Skeery Stuff

Simplicity in Kansas has a great blog and one of its recent posts discusses this infamous housing bubble - a topic so big that Ben Jones has dedicated his entire blog to the topic, over at HousingBubbleBlog.com. (The bubble is deflating if not outright bursting, by the way.)

Simplicity in Kansas has a great blog and one of its recent posts discusses this infamous housing bubble - a topic so big that Ben Jones has dedicated his entire blog to the topic, over at HousingBubbleBlog.com. (The bubble is deflating if not outright bursting, by the way.)US Debt is monitored over at the US Debt Clock. As of September 9, 2006, at 5:16:33 pm GMT, the debt was $8,533,794,901,315.96 according to the clock - and it grows $1.75 billion a DAY.

Meanwhile, the Bureau of Economic Analysis keeps track of savings. Savings have been at a negative since 2005 -- and prior to that, they hadn't been over 3% of disposable personal income since 2000. During this decade, at our best, the country was only saving 3 pennies out of every dollar.

Is all this skeery stuff news? No. MIT was calling the American economy a "Ponzi scheme" almost ten years ago - you can read the essay by F. Kreisel at MIT's site.

[Thanks to MBHunter for pointing out that the debt is growing by billions, not trillions, a day. I've edited this post accordingly. RK]

September 7, 2006

The Nest Egg Index & 12 Tips On Saving

Stockbrokerage firm AG Edwards has released its second Nest Egg Index. In it, they rank what they consider to be the 500 top-saving communities nationally.

Stockbrokerage firm AG Edwards has released its second Nest Egg Index. In it, they rank what they consider to be the 500 top-saving communities nationally.Ranking is based upon 12 factors, retirement plans and home ownership being two of them. The report reveals what parts of the country are doing well -- and not so well -- in building financial "Nest Eggs", according to the company.

934 communities are included this year, with the top five states being: New Jersey, Connecticut, Minnesota, Maryland, and Massachusetts, and the top five cities: Los Alamos, New Mexico; Bridgeport-Stamford-Norwalk, Connecticut; San Jose, California; Torrington, Connecticut; and Minneapolis-St.Paul-Bloomington, Minnesota.

In tandem with this, AGEdwards has compiled a list of 12 Tips on Savings, details on the site and headings shown below:

Start early.

Get over the planning hump.

Prioritize your long-term nest egg needs.

Pay yourself first.

Participate in employer-sponsored savings and retirement plans.

Diversify.

Control and reduce your debt.

Compare what you spend with what you want.

Monitor your savings plans and progress.

Review your income tax withholding.

Team up.

Expect the unexpected.

You can check your community online at their site as well as the criteria used for the study.

July 10, 2006

Site to See: The Ultimate Cheapskate

For those of you who don't watch the Today show, this will be news: a man named Jeff Yeager appears there regularly, dispensing frugal living tips under the nickname of the "Ultimate Cheapskate." He's also just landed a book deal with Broadway (to be published in Fall 2007), entitled "Laugh Your Assets Off: How to Spend Less and Enjoy Life More by America's Ultimate Cheapskate."

For those of you who don't watch the Today show, this will be news: a man named Jeff Yeager appears there regularly, dispensing frugal living tips under the nickname of the "Ultimate Cheapskate." He's also just landed a book deal with Broadway (to be published in Fall 2007), entitled "Laugh Your Assets Off: How to Spend Less and Enjoy Life More by America's Ultimate Cheapskate."His website is HERE if you want to check him out.

February 16, 2006

Great Money Helper

The Consumer's Almanac has a great money site. Here, you can input personal information and obtain your net worth, as well as get help planning for vacations, retirement, and the kids' college. Not the only site you'll need, but a good place to start.

The Consumer's Almanac has a great money site. Here, you can input personal information and obtain your net worth, as well as get help planning for vacations, retirement, and the kids' college. Not the only site you'll need, but a good place to start.Setting financial goals isn't the most fun thing to do, but you know you need to do it, and afterwards, to check yourself against them on a regular basis to insure you're on track.

This site helps.

February 4, 2006

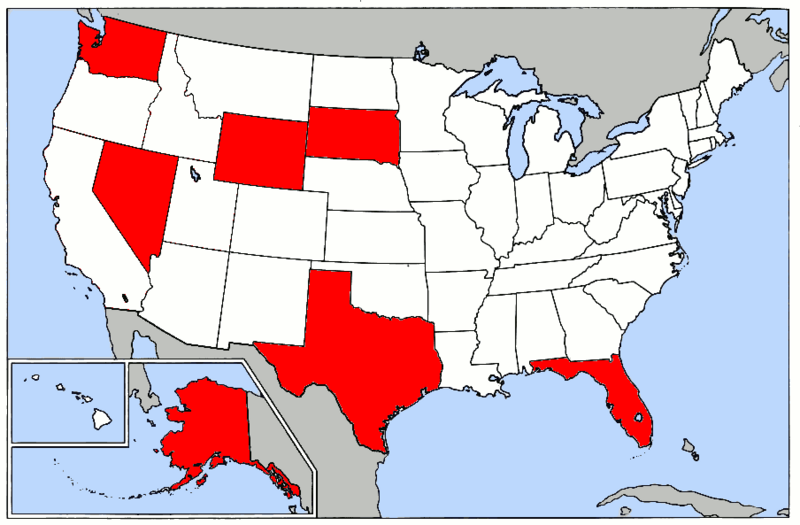

No State Income Tax

Not every state taxes the income of its citizenry. Just something to ponder if you're considering relocation. Those that don't: Alaska, Texas, Florida, Washington, Nevada, South Dakota, and Wyoming. (Two others, New Hampshire and Tennessee, only tax income from dividends and interest.)

For those that do tax, the rates vary. A comparision chart is provided at tax.admin.org.

(Those states appearing in red do not have a state income tax.)

January 20, 2006

Gold

Buying gold online has been made easy by sites such as BuillionVault, and GoldMoney.

For more information on how to invest in gold, visit WorldGoldCouncil, and for beginners, check out Gary North's article. It's excellent.

How to PIF the Mortgage ASAP

Lots of the Simplicity books (as well as those folk over at the Daily Reckoning) think renting is better than buying - but if you're already in a mortgage and want to stay there, at least pay it off as fast as you can.

How? You can make an additional payment each year, either lump sum (think bonus time, or refund time) or by paying an extra 1/12th of your monthly payment each month. If your payment is $1000, pay $1083.33 each month ($1000 divided by 12 = $83.33). At year end, you will have paid that extra month's payment. Or, you can calculate an amount to pay against principal, so you can pay the loan off in X years, and you decide the X.

Why? You save a ton of money by cutting off the interest. For details on all this math, go HERE or HERE.

How? You can make an additional payment each year, either lump sum (think bonus time, or refund time) or by paying an extra 1/12th of your monthly payment each month. If your payment is $1000, pay $1083.33 each month ($1000 divided by 12 = $83.33). At year end, you will have paid that extra month's payment. Or, you can calculate an amount to pay against principal, so you can pay the loan off in X years, and you decide the X.

Why? You save a ton of money by cutting off the interest. For details on all this math, go HERE or HERE.

Subscribe to:

Comments (Atom)